Except for Value at Risk and option pricing, quantum algorithm are not often used to solve problems in finance. Indeed, such analysis are computationally too expensive to perform on classical computers.

In this study, authors demonstrate that the sensitivity analysis of a business risk model – due for instance to external factors like political events or regulation – at Deutsche Börse Group can be implemented as a quantum program. To do so, they used Qiskit to run and present the code.

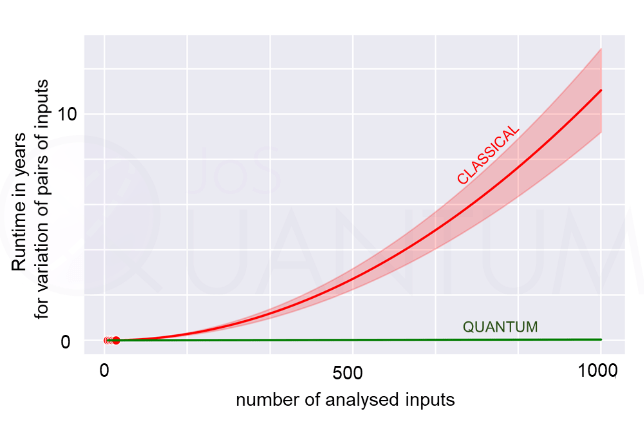

It is shown that the expected theoretical quadratic speed advantage over the classical approach, consisting of running Monte Carlo simulations for each relevant set of parameters and finding the most sensitive set, can be attained. Of course, this model can also be applied to other kinds of risks – credit, operational… –. An important fact is that only 200 quits would be sufficient to run this model, so we could guess that as soon as first quantum hardware are available this problem could be solved.

JoS Quantum uses Quantum computing to tackle new problems in finance, energy and insurance.

To learn more, find the paper here.

The post A Quantum algorithm for the sensitivity analysis of business risks appeared first on Swiss Quantum Hub.